“Permanent refinery closures since the start of 2019 reduced global capacity by around 4.7mn barrels per day, Barclays estimates, and new refinery capacity such as at Kuwait’s Al Zour can’t be brought quick enough. As a result, US and European refinery gross margins are least four times the long-run average“

Especially interesting is the long journey to getting regulators on board in the US (after years or resistance).

“One day during their time at Y Combinator, Lopes Lara and Mansour say, they cold-called 60 lawyers they’d found on Google. Every one of them said to give up”.

Fascinating read that collects several pieces of evidence to suggest “that it is increasingly challenging to make discoveries that have comparable impact to the ones in the past“.

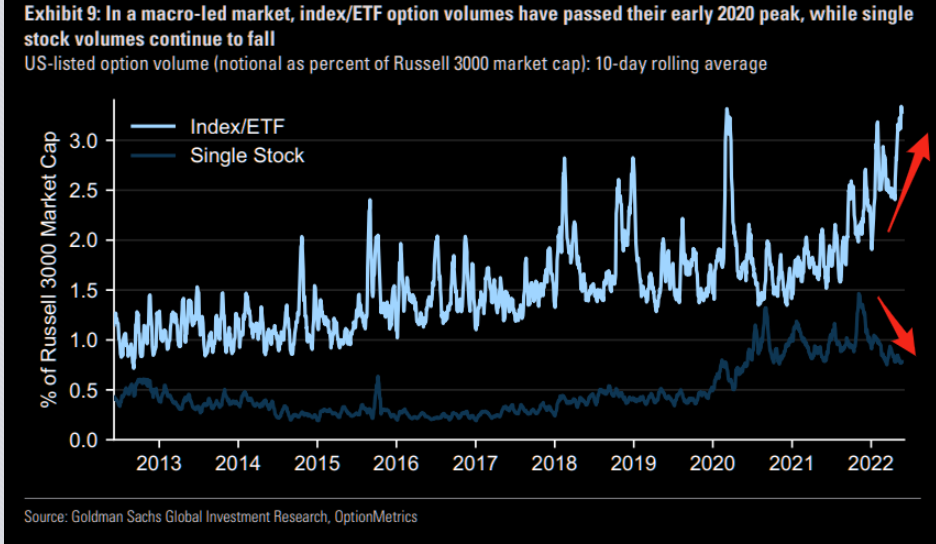

Consider this chart, for example.

It is based on all citations made to academic papers by US patents filed that year (and eventually granted in the next five years).

The chart shows the percentage of these citations that were papers published in the preceding five years.

The result – “citations to recent work have become increasingly less common“.

The rest of the evidence is in this vein, including especially interesting data on how new topics in science are stagnating. This has a nice corollary to this essay here (for progress we need novel things to work on, h/t The Diff).

Tyres are an order of magnitude worse source of particles pollution than exhausts.

“We came to a bewildering amount of material being released into the environment – 300,000 tonnes of tyre rubber in the UK and US, just from cars and vans every year.”

Whereas “Tailpipes are now so clean for pollutants that, if you were starting out afresh, you wouldn’t even bother regulating them.”

Listed tyre companies (GT, ML) are generally ranked low on ESG risk.

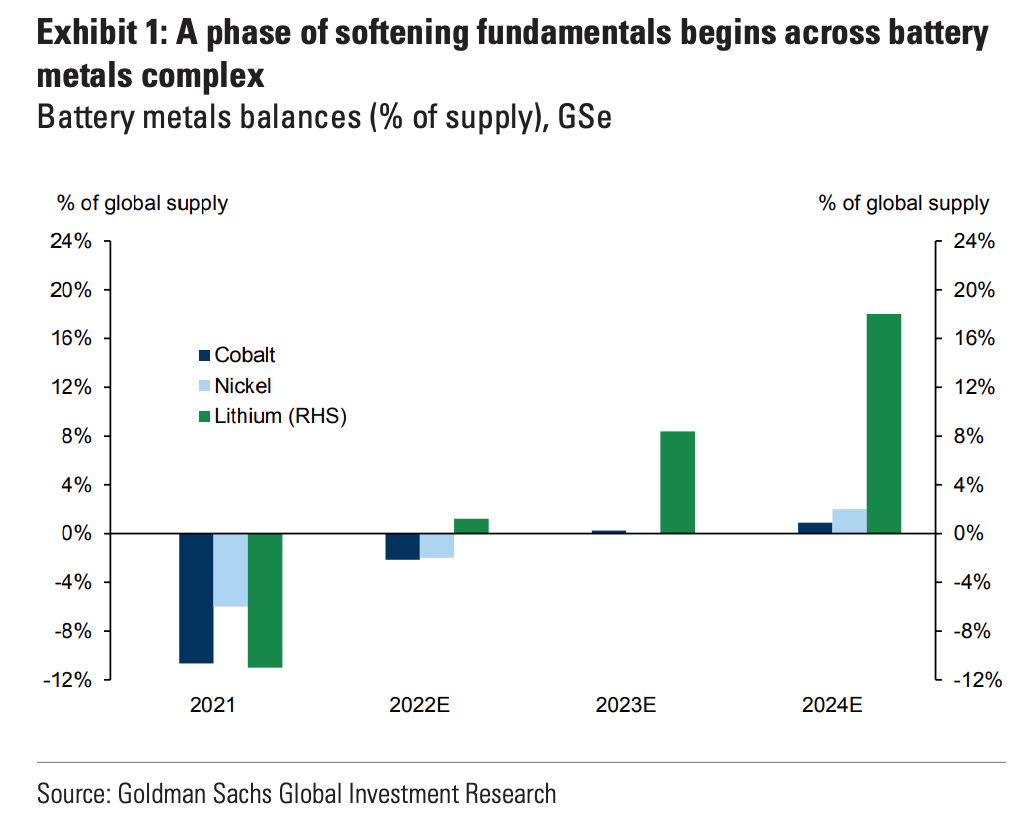

As the saying goes – the best cure for high prices is high prices.

According to GS this is now coming to battery metals (cobalt, lithium and nickel).

In other words, despite an exponential demand profile, the surge in prices is bringing on a huge supply response.

“We forecast all three metals to shift into sustained surplus over the next 1-2 years” (see chart).

“Lithium is the most prominent in this trend, where we expect supply growth to average just over 30% per year over 2022-25, reflecting the ramp-up of new projects in Australia, China and Chile in particular.”

Interesting argument by an ex FT/FTAV journalist, who has recently started her own newsletter, on why she didn’t chose Substack.

One thing that stood out is legal cover. “As it stands, Substack can shift the biggest risk and cost in all journalism — libel risk — onto the shoulders of individual authors.”

This ties in with news they have dropped their Series C round (at a valuation of $750m – $1bn).

The reason is likely down to the fact they made only $9m of revenue last year, suggesting even their previous valuation of $650m is too high.

The other thing is moderation – as any platform grows moderation becomes an issue, something other publishers have been quick to point out.

This was a fascinating read on why some technologies linger and hence have a much longer tail than the market often predicts.

The reason – “cultural forces create market demand even if supply is available more efficiently (even infinitely) elsewhere“. In some cases (not obviously just related to age) the perceived value actually increases.

Think about movie theaters surviving despite the rise of home cinema. Why? The social value of gathering at the movies.

Or enjoying the slow deliberate read of a newspaper.

Or the demand, sometimes sinister, for the near 5 million payphone calls made each year in the UK.

Decline is inevitable but not in all cases (booming vinyl sales for example).

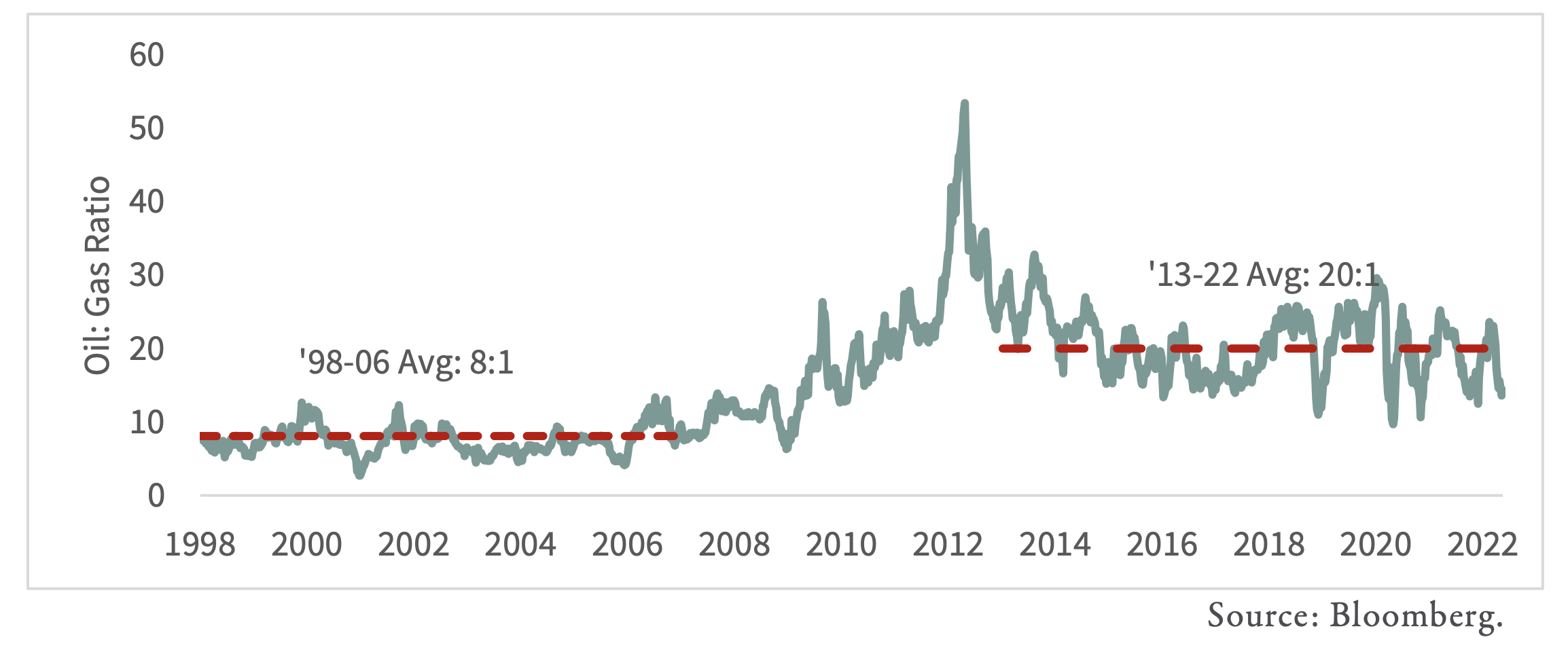

Before shale took off oil to gas prices averaged 8 to 1 – close to their energy equivalence ratio.

Since 2013 this ratio has averaged 20 to 1.

Outside of North America the ratio is 3 to 1.

“In other words, US gas is priced at an energy-equivalent discount of 56% to world oil and a 77% discount to world gas. In our 35 years investing in global energy markets, we have never seen such a wide disparity.“

Source (including arguments on why it might revert).

Astral Codex Ten picks up on an expanded nootropics recommendation data set.

The results are in this table and show three things (1) addictive/illegal is preferred to safe (2) difficult but popular > chemicals (3) high tech > normal.

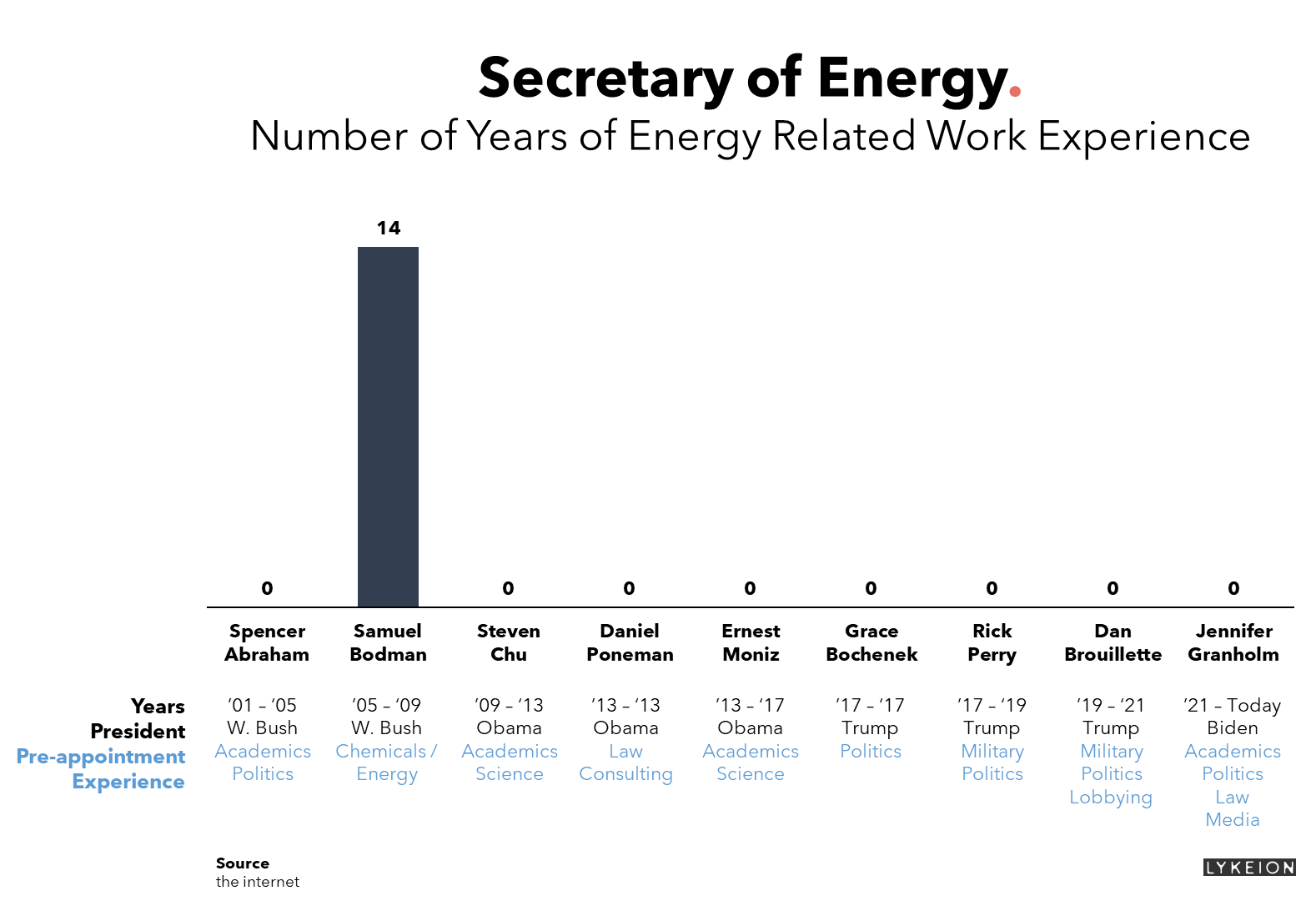

“Over the last 20 years, across four Presidents (two Republicans and two Democrats) we have had exactly one energy secretary with any real-world energy experience before they were brought into the President’s cabinet.“